The financial framework supporting the economy relies heavily on monetary policy tools to ensure stability, control inflation, and foster economic growth. Among the key components of monetary policy is the repo rate, which plays a crucial role in determining loan interest rates and impacts the broader economic conditions. Alongside it, the reverse repo rate is another important monetary tool. In this article, we will delve into the concept of the repo rate, its relationship with loan interest rates, the reverse repo rate, and its significance in the financial ecosystem.

What Is the Repo Rate?

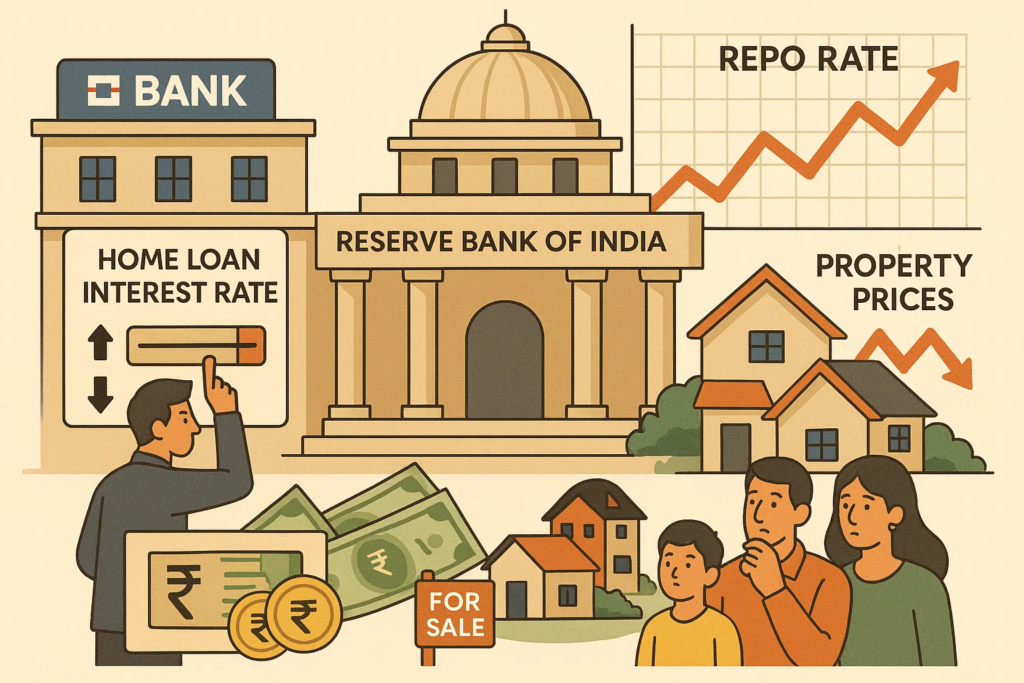

The term repo rate is short for “repurchase rate.” It is the rate at which the central bank of a country, such as the Reserve Bank of India (RBI), lends money to commercial banks for short-term borrowing. In other terms, it is the rate at which commercial banks borrow funds from the central bank by selling securities.

During times of liquidity crunch, commercial banks approach the central bank to meet their temporary monetary requirements. The central bank provides funds to these commercial banks in exchange for government securities as collateral. The rate of interest charged on this borrowing is the repo rate.

The repo rate is a critical monetary policy tool for controlling inflation, stabilizing the economy, and ensuring adequate liquidity in the financial system.

What Is the Reverse Repo Rate?

To fully understand the repo rate, it is essential to comprehend its counterpart—the reverse repo rate. While the repo rate defines the rate at which commercial banks borrow money from the central bank, the reverse repo rate refers to the interest rate at which the central bank borrows money from commercial banks.

When commercial banks have excess funds, they often park them with the central bank to earn interest. This helps the central bank to absorb liquidity from the banking system and control inflation.

Together, the repo rate and reverse repo rate form the foundation of monetary policy and influence liquidity in the economy. Any change in these rates has a ripple effect across the financial system, particularly in terms of loan interest rates and lending activity.

How Does the Repo Rate Work?

The repo rate involves a short-term borrowing agreement. Here’s how it operates:

Liquidity Requirements

When commercial banks face a shortage of funds or liquidity, they approach the central bank to borrow money to meet their needs.

Collateral Submission

The central bank provides funds to the bank, but in return, the borrowing bank has to pledge securities like government bonds as collateral.

Repurchase Agreement

As part of the agreement, the borrowing bank agrees to repurchase the securities at a predetermined price after a specified period.

The cost of borrowing this money is determined by the prevailing repo rate. Naturally, any increase or decrease in the repo rate directly impacts borrowing costs for banks and subsequently influences interest rates for loans offered to businesses and individuals.

How Repo Rate Impacts Loan Interest Rates

The repo rate has a direct correlation with loan interest rates offered by commercial banks. Let us explore how changes in the repo rate influence the borrowing costs of consumers:

Repo Rate Hike Leads to Higher Loan Rates

When the central bank increases the repo rate, borrowing money from the central bank becomes more expensive for commercial banks. To compensate, banks increase the interest rates on loans to customers, making borrowing costlier. This is usually done to curb inflationary pressures in the economy.

For instance, if the central bank notices rising inflation due to excessive borrowing or spending, it may implement a repo rate hike to reduce liquidity in the system. Higher borrowing costs often translate into lower consumer spending, which helps control inflation.

Lower Repo Rate Makes Loans Affordable

Conversely, when the repo rate is reduced, borrowing from the central bank becomes cheaper for commercial banks. This allows banks to provide loans to their customers at lower interest rates, thereby encouraging borrowing and boosting economic activity.

A lower repo rate is typically implemented when the central bank aims to revive growth or stimulate demand in the economy during periods of slowdown or recession.

Role of Repo Rate in Monetary Policy

The repo rate plays a pivotal role in achieving monetary policy objectives such as controlling inflation, promoting growth, and maintaining liquidity. Central banks make strategic repo rate changes based on the macroeconomic conditions, current inflation rates, and the economy’s growth trajectory.

Inflation Control

When inflation is high, central banks implement a tight monetary policy, increasing the repo rate. This discourages excessive borrowing and spending, subsequently reducing inflationary pressures.

For example, in situations of excessive demand for goods and services, central banks use the repo rate to limit liquidity, encouraging people to save rather than spend.

Boosting Economic Growth

When the economy experiences a slowdown, central banks reduce the repo rate to lower borrowing costs. This encourages businesses to take loans, invest, and expand their operations. Similarly, consumers can borrow at lower interest rates, leading to increased spending and a revival of economic activity.

Liquidity Regulation

The repo rate ensures that banks have sufficient liquidity to meet their daily operational requirements. By increasing or decreasing the repo rate, central banks fine-tune the liquidity available in the banking system, ensuring stability and financial support.

Importance of the Reverse Repo Rate

While the repo rate determines the borrowing costs for banks, the reverse repo rate influences how commercial banks park their funds. Here’s why the reverse repo rate matters:

-

When the reverse repo rate is increased, banks find it more lucrative to deposit their surplus funds with the central bank, earning higher interest. This reduces the liquidity in the economy, as less money is available for lending or investing.

-

If the reverse repo rate is lowered, banks are encouraged to lend money to businesses and consumers instead of parking funds with the central bank. This increases money circulation in the economy and drives spending and investment.

Both the repo rate and reverse repo rate work in tandem to regulate liquidity and ensure macroeconomic stability.

Repo Rate Vs Reverse Repo Rate

Understanding the difference between repo rate and reverse repo rate is essential for grasping their impact on the economy:

Recent Trends in Repo Rate Decisions

Central banks periodically announce changes to the repo rate based on economic indicators like inflation, employment, GDP growth, and fiscal policies. These changes are dictated by complex analyses of macroeconomic trends.

For instance, during the COVID-19 pandemic, several central banks adopted a low repo rate policy to minimize the burden on borrowers and businesses. However, as inflationary pressures surged globally in 2022 and 2023, central banks including the US Federal Reserve and India’s RBI resorted to incremental repo rate hikes to stabilize inflation and normalize economic activities.

It is crucial to monitor repo rate policy decisions as they directly affect financial planning, investments, and borrowing costs for individuals and businesses alike.

Conclusion

The repo rate is one of the most significant monetary tools that central banks utilize to shape economic conditions. Its impact on loan interest rates underscores its importance in the daily lives of individuals and businesses. Whether the repo rate is raised or lowered, it influences borrowing power, spending patterns, and overall economic activity.

The reverse repo rate, also pivotal in monetary policy, complements the repo rate by absorbing surplus liquidity and controlling inflation. Together, these rates maintain balance in the economy and serve as levers to address fluctuations and challenges in the financial system.

In a world driven by economic activities, understanding the repo rate’s meaning and its implications on loan interest rates equips individuals and businesses with insights to make sound financial decisions. Monitoring repo rate changes announced by central banks can help one adapt to economic changes, navigate credit markets, and plan finances prudently. As monetary policies continue to evolve, studying the dynamics of the repo rate remains essential for developing a robust understanding of the macroeconomic ecosystem.